Basmati exports: goodbye depreciation fever?

Published on: June 23, 2021.

Filed under:

Monthly foreign trade report card for May 2021 is full of surprises. Rice exports, which were expected to chart fresh heights on the back of global commodity price boom, have fallen by nearly half to almost a hundred thousand dollars for the month. In fact, monthly rice exports are second lowest in at least 32 months, even lower than the low base effect from last year May that coincided with peak pandemic period.

Although trade performance during a single period is never sufficient to extrapolate long-term trends, much of these developments have been long in the making. Readers will recall that rice exports were hailed as a saviour – after textiles – for Pakistan’s dismal export performance just two years ago. There is little doubt that Pakistan’s rice export rebounded substantially post massive currency depreciation circa 2018-2019, the recovery in export volumes was always bound to run out of steam. Here is why.

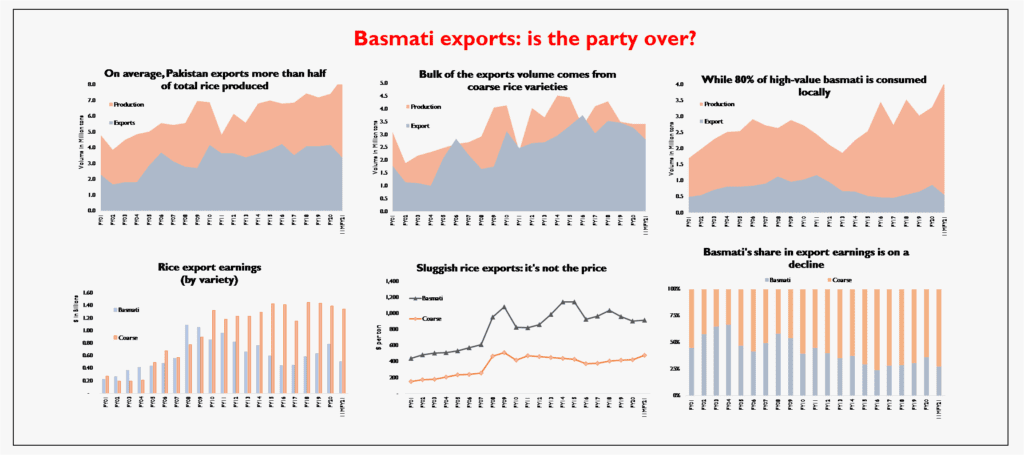

As most commoditized goods exports go, Pakistan’s rice processors also benefited from the newfound price competitiveness following currency depreciation. Although total export volume remained annoyingly stubborn at 4 million tons per annum, quality of exports improved. Export mix began to shift back towards high value basmati rice, which are valued nearly twice in unit price than the coarse rice variety that forms bulk of total exports (over 80 percent of volume, and 70 percent of value).

But after two years of bull run, the recovery witnessed in basmati exports is stalling. A deeper dive through granular data points to two possible explanations for the replay of basmati stagnation. First, the global basmati export market (excluding subcontinent) is sized at roughly 5 million tons per annum, mostly consisting of Iran, Gulf, and desi diaspora in North America and European continents. Historically, exporters based out of India have had a commanding export market share, averaging over 80 percent.

Unlike Pakistan, basmati is not considered a staple rice variety in India, especially outside of north Indian states. Thus, India produces a much larger exportable surplus of basmati, and has long established internationally recognized brands. In fact, basmati exports contribute 60 percent of total rice export earnings for the neighbour, whereas the figure stands at just one-third for Pakistan. Indian exporters also enjoy better price competitiveness (although Indian-origin basmati has witnessed bans by EU due to high tricyclazole levels in recent years).

Thus, despite its high-unit value potential, Pakistan’s basmati exports face a natural ceiling due to limited demand from exporting destinations, and dominant competitor market position. But there may be another centrifugal force at work, that’s limiting the upside potential of basmati exports.

While basmati’s export potential is often celebrated at the policy level, as much as 80 percent of total basmati rice produced domestically is geared towards local consumption. Moreover, the trend towards local consumption has only been inching forward in recent years, rising to as much as 85 percent in FY21.

Although basmati may have long been a national favourite for biryani and pulao, it appears that exogenous variables may also be driving increasing local demand for the variety. For one, growth in production of Pakistan’s staple cereal crop – wheat – has remained stunted, and has failed to keep up with rising domestic population. Two, although globally rice is considered an inferior grain to wheat, that’s not the case for basmati, which is considered premium due to its aromatic qualities. Three, although basmati may be more expensive, but low-mechanization means that the harvested crop is often of poor quality and has a high share of rice in broken form, that sells at lower price points in domestic market, but has little foreign demand. And finally, while the per unit price of rice may be higher than that of wheat flour, one kilogram of cooked rice feeds as many as 10 – 15 people, much higher than the number of flatbreads that may be prepared by a kilogram of flour.

Turns out as Pakistan’s population grows, rice – specifically basmati – is fast becoming the more affordable cereal. Meanwhile, the static export volume of coarse rice varieties keeps the illusion of rice export potential alive. But if coarse rice is cheaper than basmati, why does it not substitute basmati in local diet?

Two reasons. While coarse rice output consists nearly half of national rice production, it is actually grown using imported varieties that are alien to local tastes and food recipes. Three-fourths of domestic coarse rice production takes place in the saline backwaters of Sindh, where basmati cannot be grown. Instead, hybrid rice is deeply popular in the southern province due to its high yielding varieties that have earned better profits to farmers over last two decades due to demand by exporters.

Meanwhile, while domestic basmati demand may be rising, the variety can only be grown in Punjab province due to unique soil and climatic conditions required. This means that basmati – which is already a low-yielding expensive crop – has limited cultivable area available to it.

What does this mean for rice export performance? Mainly that while the “unexploited potential of basmati exports” may look like a not-to-miss opportunity, higher domestic demand will keep it from ever reaching fruition. Although massive currency devaluation during 2019 made basmati export highly lucrative, that may have been a fleeting opportunity that has since disappeared, especially due to rising domestic prices. Like all businesses, basmati processors are opportunistic traders, who took advantage of better returns in international market due to currency volatility two years ago. But they may have little reason to continue selling to high maintenance, foreign buyers when the voracious appetite of domestic buyers remains unsatiated.